What is PCP car finance?

Personal Contract Purchase — PCP — is the UK’s most popular way to finance a car. More than 80% of new cars bought through a dealership are funded by PCP, and it’s increasingly common on quality used cars too.

But for all its popularity, PCP remains genuinely confusing. Balloon payments, GMFV, mileage caps, positive equity — the jargon alone is enough to put people off. This guide strips all of that away and explains exactly how PCP works, what it costs, and whether it’s the right choice for you.

What is PCP finance?

PCP stands for Personal Contract Purchase. It’s a type of secured car finance where you borrow money to cover the depreciation of a vehicle over an agreed term — typically 24 to 48 months — rather than its full purchase price.

You pay a deposit up front, make fixed monthly payments throughout the contract, and then face a choice at the end: buy the car outright by paying a final lump sum (the balloon payment), hand it back, or use any equity to move into a new car.

The key thing that separates PCP from hire purchase (HP) is that you’re not paying off the full value of the car month by month. You’re only paying for the portion of the car’s value it’s expected to lose during your contract. That’s why monthly payments are typically lower with PCP than with HP — but it also means you don’t automatically own the car at the end.

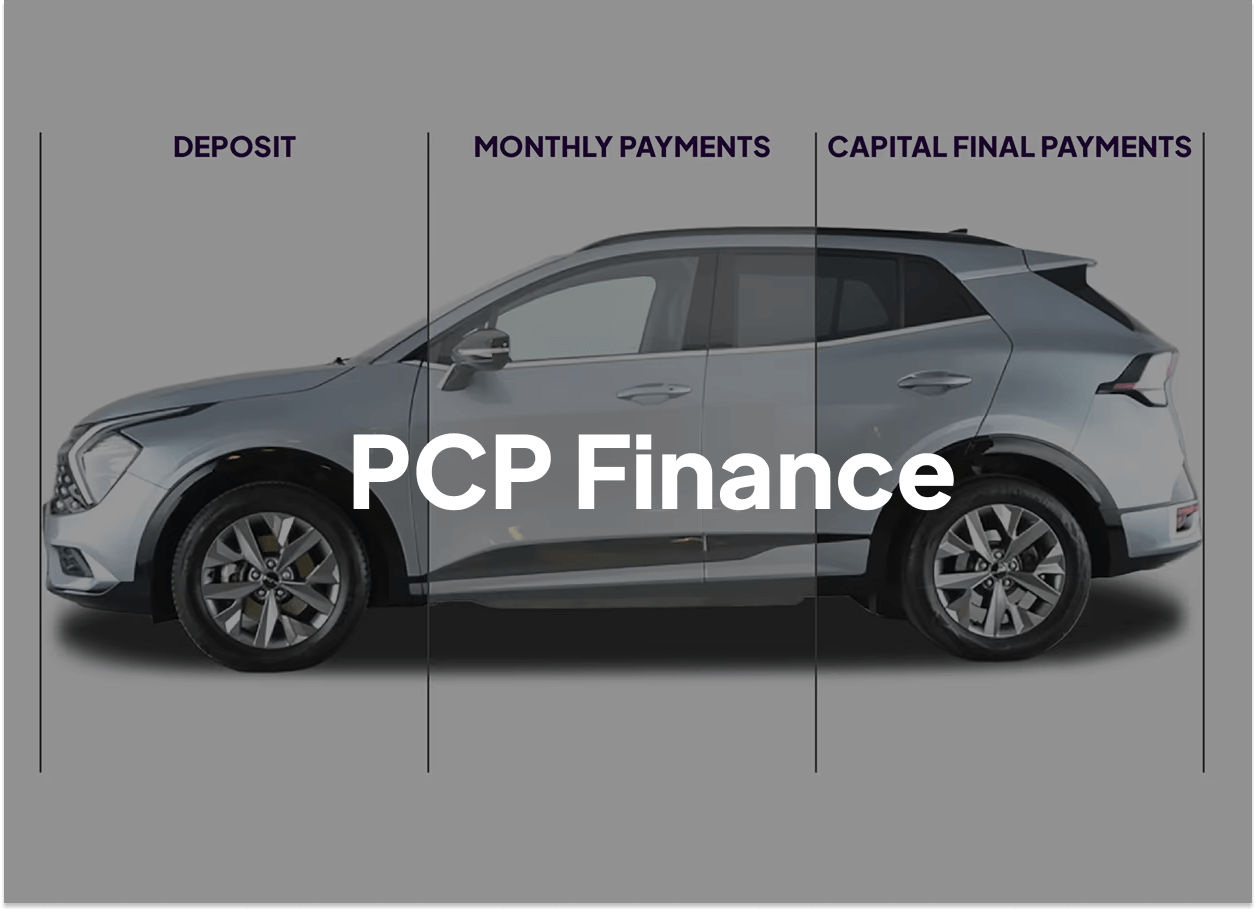

How does PCP work? A step-by-step breakdown

Step 1 — Your deposit

Most PCP agreements require a deposit of around 10% of the car’s value, though you can put down more (up to around 40%) to reduce your monthly payments. Your deposit can be paid in cash or by using your current car as a part exchange.

At Carsa, our team can help you understand exactly how your part exchange value translates into your deposit — removing one of the most stressful parts of the buying process.

Step 2 — The amount you borrow (and your monthly payments)

The lender looks at the car’s current value and estimates what it will be worth at the end of your contract. The difference between those two figures is what you’re financing — that’s called the depreciation.

For example: a car worth £15,000 today might be expected to be worth £9,000 in three years. Your monthly payments cover that £6,000 gap, plus interest at the agreed APR.

This is why PCP payments are lower than HP payments on the same car — you’re not financing £15,000, you’re financing £6,000.

Step 3 — The Guaranteed Minimum Future Value (GMFV)

The GMFV — also called the balloon payment — is the lender’s guaranteed estimate of what your car will be worth at the end of the term. It’s locked in at the start of your agreement.

This matters for two reasons. First, if you want to keep the car, it’s the amount you’ll need to pay at the end (plus a small option-to-purchase fee, typically around £10). Second, if the car’s actual market value is higher than the GMFV when your contract ends, you have positive equity — and you can use that as a deposit on your next car.

Step 4 — Your three choices at the end

When your PCP contract ends, you have three options:

- Buy the car — Pay the balloon payment (GMFV) plus the option-to-purchase (OTP) fee. The car is yours outright.

- Hand it back — Return the car to the finance company with nothing more to pay, provided you’ve stayed within the mileage limit and there’s no damage beyond fair wear and tear.

- Part-exchange into a new car — If the car is worth more than the GMFV, you have equity. Use it as a deposit on your next vehicle and start a new agreement.

PCP, HP and Personal Contract Hire — what’s the difference?

PCP finance: advantages and disadvantages

Understanding the balloon payment

The balloon payment — formally called the Guaranteed Minimum Future Value (GMFV) — is the single most important figure in any PCP agreement. It’s the lender’s estimate of what your car will be worth at the end of your contract.

It’s set in stone at the start of your agreement, which means:

- If the car’s actual market value drops below the GMFV, you can simply hand it back. The lender takes the hit — not you.

- If the car’s actual market value stays above the GMFV, you have positive equity. You can use that as a deposit on your next vehicle.

Cars with strong residual values — typically premium brands, popular hatchbacks, and low-mileage examples — tend to generate positive equity more often. This is one reason well-priced used cars from a trusted source like Carsa can be particularly good candidates for PCP finance.

If you choose to buy the car at the end, you’ll also pay an option-to-purchase (OTP) fee on top of the GMFV. This is usually a nominal amount — often around £10, though some lenders charge up to £200.

What affects your PCP monthly payment?

Five factors determine what your monthly PCP payment will be:

- The car’s purchase price — The more expensive the car, the more there is to depreciate.

- Your deposit — A larger deposit reduces the amount you’re financing and lowers your monthly payments.

- The GMFV — A higher GMFV (i.e. a car that holds its value well) means less depreciation to finance, which means lower monthly payments.

- The APR — Your interest rate, based primarily on your credit score. At Carsa, finance is available from 8.9% APR representative.

- The contract length — Spreading the payments over 48 months rather than 24 reduces monthly cost but increases total interest paid.

What do you need to qualify for PCP finance?

To apply for PCP finance you’ll typically need to:

- Be at least 18 years old

- Be a UK resident

- Have a regular, provable income

- Pass a credit check (a hard search will be carried out)

A strong credit score gives you access to the most competitive APR rates. If your credit history is less than perfect, you may still be accepted — but the interest rate offered may be higher, or you may need a larger deposit.

It’s worth checking your credit report with Experian, Equifax or TransUnion before applying so there are no surprises. Carsa’s finance team can walk you through your options in plain English — no pressure, no jargon.

How does PCP affect your credit score?

When you apply for PCP finance, the lender carries out a hard credit search. This shows up on your credit file and can be seen by other lenders. Making multiple applications in a short period can dent your score — so avoid scattergun applications across different providers.

Once accepted, PCP can actually help your credit score over time. Every on-time payment is recorded as positive behaviour on your credit file, demonstrating financial reliability to future lenders.

On the other hand, missed or late payments are also recorded — and can seriously harm your score, reducing your ability to access credit in the future. Always make sure the monthly payments are comfortably within your budget before signing.

Can you end a PCP contract early?

Yes — in two ways.

Within 14 days of signing: You have a statutory cooling-off period. You can cancel the agreement and return the car with no penalty.

After 14 days — Voluntary Termination: Under Section 99 of the Consumer Credit Act 1974, once you’ve paid at least 50% of the total amount payable (this includes the balloon payment in the calculation), you can voluntarily terminate the agreement and return the car. You won’t owe any further monthly payments, though the car must be in reasonable condition.

Settling early: You can also request a settlement figure from the lender at any time. Pay this and the car is yours — the finance is cleared.

Is PCP right for you?

PCP tends to work well if you:

- Want lower monthly payments and don’t need to own the car from day one

- Like the idea of changing your car every two to four years

- Drive a predictable, manageable annual mileage

- Want flexibility about what happens at the end of the contract

PCP may not be the right fit if you:

- Cover very high annual mileage — the penalties for exceeding agreed limits can be significant

- Want guaranteed ownership without a large end-of-term payment

- Plan to modify the car (you can’t while it’s on finance)

- Prefer a simple, one-and-done repayment structure — in which case HP or a personal loan may suit you better

PCP finance at Carsa

Every car at Carsa is available through flexible finance options — including PCP — with rates from 8.9% APR (11.9% APR representative). Our stock is priced on average £700 below market value, checked daily to stay competitive, and every vehicle goes through a comprehensive mechanical and cosmetic inspection at our dedicated preparation centre before you see it.

You can browse our full stock online, reserve the car you want, and collect from your nearest Carsa store — or speak to our team by phone if you’d prefer to talk it through first. No pushy sales, no hidden fees, no haggling required.

All cars come with a 90-day warranty as standard, with the option to upgrade to Platinum Cover for extra peace of mind.

Related articles

Ready to find your next car?

Browse hundreds of expertly prepared used cars — all fully checked, cleaned, and ready to drive away.

Talk to us, anytime.

Our friendly team is just a message or call away.

Message us on whatsapp, 24/7